The Balanced Scorecard (BSC) emerged in response to the shortcomings of traditional financial control systems. Some scholars argued that traditional financial control had ceased to evolve since 1925, which resulted in management focusing more heavily on costs than on other dimensions of performance (Mark W. Rieman, 2003, pp. 2–7).

The Balanced Scorecard (BSC) emerged in response to the shortcomings of traditional financial control systems. Some scholars argued that traditional financial control had ceased to evolve since 1925, which resulted in management focusing more heavily on costs than on other dimensions of performance (Mark W. Rieman, 2003, pp. 2–7).

As change factors developed and complexity increased after World War II, managerial decisions became strongly influenced by financial indicators. However, these indicators failed to provide proper long-term strategic guidance. Consequently, the 1980s witnessed the emergence of several managerial concepts and tools such as Total Quality Management (TQM), Kaizen, Business Process Reengineering, and others (Al-Maghribi, 2006, p. 189).

The idea of evaluation through the Balanced Scorecard is linked to extensive consulting experience, as organizations were required to overcome challenges in the business environment by shifting their thinking toward multiple performance dimensions. This enabled them to enhance sustainability and satisfy various stakeholders.

The emergence of the Balanced Scorecard resulted from accumulated knowledge and consulting expertise led by several researchers in the early 1990s. Kaplan and Norton are considered the pioneers of the Balanced Scorecard concept. The most important managerial intellectual trends that accompanied its development include (Idris, 2009, p. 145):

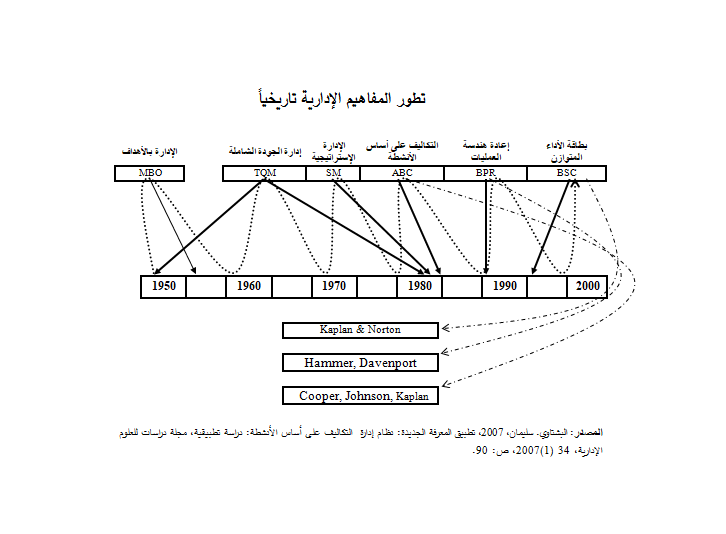

It is noteworthy that the Balanced Scorecard is the outcome of a historical evolution in management concepts, starting with Management by Objectives (MBO) and Total Quality Management, moving through Activity-Based Costing and Business Process Reengineering, and culminating in comprehensive evaluation using the Balanced Scorecard (Al-Bashtawi, 2007, p. 90).

Customer focus, reliance on real data, internal processes, proactive management through advance planning, unlimited participation, and continuous improvement constitute the core pillars of the Balanced Scorecard as an integrated system aligned with Six Sigma applications in quality management (Al-Sulaimeh, 2007, p. 35).

Since Kaplan and Norton introduced the Balanced Scorecard, several changes have occurred. Three main generations can be identified (Al-Jizan, 2008, p. 121):

The Balanced Scorecard is described as a matrix based on four perspectives for performance measurement without strong cause-and-effect relationships among the dimensions and their indicators.

This generation emerged to address the problems of the first generation. It focused on linking objectives with selecting measures that best align with these objectives. However, it suffered from ambiguity regarding who determines strategic objectives.

Known as the generation of strategy maps, it asserts that the Balanced Scorecard cannot function as a strategic management tool without strategy maps, which represent a clear description of strategy derived from a well-defined vision and mission.

The first application of the Balanced Scorecard was at Analog Devices in 1987. Additional dimensions such as delivery speed, process quality, and effectiveness of new service development were incorporated alongside financial measures, forming the basis of innovative balanced measurement systems (Idris, 2009, p. 141).

The Balanced Scorecard model includes financial measures that reflect past performance outcomes and integrates them with non-financial measures related to customer satisfaction, internal processes, innovation, and learning (Kaplan & Norton, 1992, p. 71).

Ho and McKay define the Balanced Scorecard as a strategic management and performance measurement system that translates organizational vision and strategy into a balanced set of integrated performance measures (Shih & McKay, 2002, p. 1).

The Balanced Scorecard represents an integrated framework for strategic performance measurement by combining financial and non-financial measures as outputs and performance drivers, linking future-oriented indicators with historical and current indicators within a causal chain across four perspectives: financial performance, customer relationships, internal processes, and learning and growth (Mark W., 2003, p. 16).

Other scholars view the Balanced Scorecard as a comprehensive set of indicators that provide senior managers with a clear picture of organizational performance, allowing organizations to select suitable indicators based on their needs and leadership priorities (Lan & Gavin, 2002).

Kaplan and Norton (1996) expanded the definition to describe the Balanced Scorecard as a system that translates strategy into a shared language understood by all employees and aligns individual and organizational objectives.

Most traditional evaluation methods relied primarily on financial indicators. However, changes in the business environment revealed their limitations, as they are historical in nature and ignore strategic information related to quality, human resource development, R&D, and customer satisfaction (Angela et al., 2007).

The Balanced Scorecard therefore serves to:

Some researchers also propose a fifth perspective: environmental and social performance.

Organizations that adopted the Balanced Scorecard achieved substantial benefits in achieving their strategic visions and satisfying stakeholders. Harvard Business Review (1992) ranked the Balanced Scorecard among the top fifteen management concepts.

Its importance includes:

The concept of “balance” reflects the integration between financial and non-financial measures, short-term and long-term objectives, and internal and external perspectives (Atkinson et al., 1997).

Time Dimension: Past, present, and future performance.

Strategic Dimension: Linking operational control with long-term strategy.

Environmental Dimension: Internal and external stakeholders.

Each perspective includes:

Functions:

Characteristics:

Performance represents the combined efforts of management and employees. Effective performance management requires a comprehensive system aligned with organizational strategy (Payant, 2006).

Performance management differs from performance appraisal; it is an ongoing process involving continuous planning, feedback, training, and development (Kotter & Heskett, 1992).

According to UCSD Human Resources, performance management is a continuous communication process involving:

Performance management enhances organizational effectiveness and aligns individual and organizational goals (Armstrong & Baron, 1998).

The gap between actual and desired performance represents the main managerial challenge. Closing this gap requires improving actual performance rather than lowering standards.

Performance results from the interaction between behavior and achievement. Ineffective behaviors should be corrected or eliminated.

Performance is influenced by:

Performance = KSAs + Motivation + Environment

Major models include:

Strategic performance management translates vision and strategy into measurable results through indicators, targets, measurement processes, and feedback mechanisms.

Dr. Abdulrahman Aljamouss, PhD is a strategic consultant, academic, trainer, and author with over 20 years of professional experience in workforce development, leadership capability building, and institutional transformation. He partners with organizations to design future-ready strategies, develop leadership pipelines, and deliver measurable, sustainable impact.

Dr. Abdulrahman Aljamouss, PhD is a strategic consultant, academic, trainer, and author with over 20 years of professional experience in workforce development, leadership capability building, and institutional transformation. He partners with organizations to design future-ready strategies, develop leadership pipelines, and deliver measurable, sustainable impact.

© Copyright - Dr. Abdulrahman Aljamouss, PhD

Powered & Designed with by Synapze

Dr. Abdulrahman Aljamouss, PhD is a strategic consultant, academic, trainer, and author with over 20 years of professional experience in workforce development, leadership capability building, and institutional transformation. He partners with organizations to design future-ready strategies, develop leadership pipelines, and deliver measurable, sustainable impact.